If you use a truck to power your livelihood, insurance is likely one of your largest fixed costs. For those in the agricultural sector, a common question arises: Is farm truck insurance cheaper than standard commercial or personal policies?

The short answer is yes. In most cases, farm truck insurance is significantly more affordable, often saving owners 30% to 60% compared to standard commercial trucking rates. However, qualifying for these lower rates depends on how you use the vehicle and where you drive it.

Why is Farm Truck Insurance Cheaper?

Insurance is all about risk assessment. Carriers offer lower premiums for farm trucks because they are viewed as "lower risk" for several key reasons:

-

Limited Mileage: Unlike long-haul commercial trucks that drive cross-country year-round, farm trucks are often used seasonally or for shorter distances (typically within a 150-mile radius).

-

Rural Operation: Driving on private farmland or quiet rural roads carries a lower statistical probability of high-speed multi-vehicle accidents compared to highway hauling.

-

Exempt Commodities: Transporting "exempt" agricultural goods (like grain, livestock, or silage) is often viewed as lower risk than hauling hazardous materials or high-value electronics.

-

Lower Liability Exposure: Many farm trucks spend the majority of their time off public roads, which reduces the likelihood of third-party liability claims.

Farm Truck vs. Commercial Truck Insurance: Price Comparison

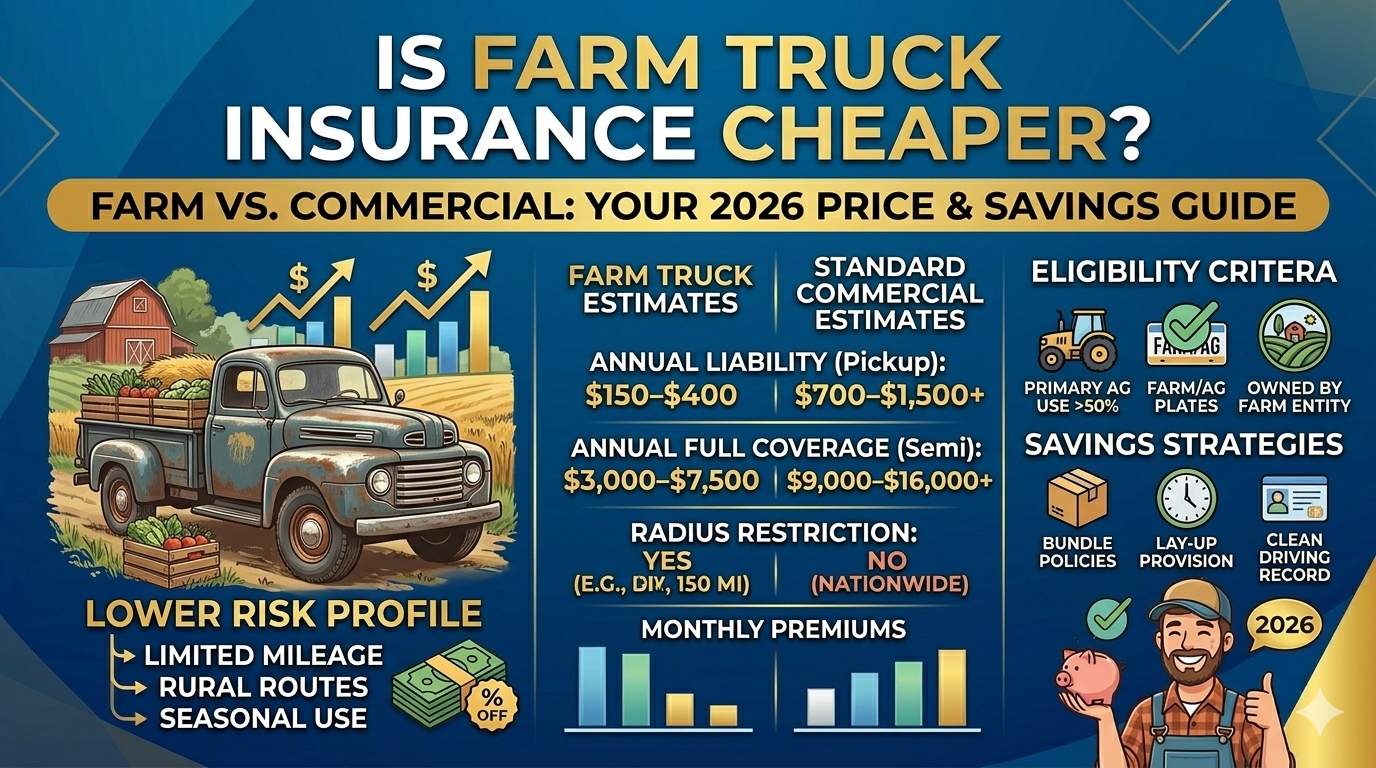

To understand the savings, look at the average annual premiums for 2026:

| Coverage Type | Farm Truck Rate (Estimated) | Commercial Truck Rate (Estimated) |

| Basic Liability | $150 – $400 | $700 – $1,500+ |

| Full Coverage (Semi) | $3,000 – $7,500 | $9,000 – $16,000+ |

| Light Pickups | Under $1,000 | $1,500 – $3,000 |

Note: These are national averages; your specific state and driving record will influence the final quote.

Do You Qualify for Farm Rates?

Simply owning a farm doesn’t automatically lower your bill. To get the cheaper "Farm Use" designation, you usually must meet these criteria:

-

Primary Use: The vehicle must be used primarily (usually 50% or more) for farm-related tasks like hauling crops, livestock, or feed.

-

Ownership: The truck is often required to be owned by the farm operator or a farm-related entity (like an LLC).

-

Radius Restrictions: Many farm policies include a "radius of operation" (e.g., 50 to 150 miles). If you haul goods across state lines for hire, you will likely be moved to a more expensive commercial policy.

-

Farm Plates: While not always mandatory for insurance, having "Farm" or "Ag" plates from your state's DMV is a strong indicator of eligibility for discounted rates.

How to Lower Your Farm Truck Insurance Even Further

If you want to maximize your savings in 2026, consider these three strategies:

-

Bundle Your Policies: You can often save 10–20% by bundling your truck insurance with your "Farmowners" or ranch policy.

-

The "Lay-up" Provision: If you only use your truck during harvest season, ask about a lay-up period. You can reduce coverage (and cost) during the months the truck is in storage.

-

Clean MVR: Even with a farm discount, a single DUI or major speeding ticket can hike your rates by 25% or more.

The Bottom Line

Is farm truck insurance cheaper? Absolutely. By switching from a standard commercial policy to a specialized agricultural policy, you can keep more money in your operation. Just ensure you are honest about your "personal use" versus "farm use" to avoid a denied claim in the event of an accident.